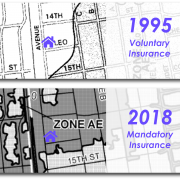

Your flood zone changed because FEMA updated your flood map due to natural and man-made events that occur over time. FEMA flood map updates are published 26 times a year and could cause you to pay higher or lower insurance premiums, pay insurance for the first time, or remove the insurance requirement from your property. You cannot stop a flood, but you can rebuild your life afterward when you are insured by the federal government or a private market policy that your loan servicer must accept.

Normal