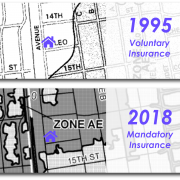

FEMA Flood Zones and the Mandatory Purchase Requirement

This article is written to aid the general public in understanding the mandatory purchase requirement and FEMA’s flood zone designations. It describes the FEMA zones and the mandatory purchase requirement at a high level and provides some details for those who have interest in nuances.